After an automobile accident, navigating the aftermath can be overwhelming. Understanding what auto insurance agencies expect from you can help streamline the claims process and ensure a more favorable resolution. This article aims to answer some of the most commonly asked questions regarding auto insurance claims following a crash.

Gather Pertinent Information

When you report a crash to your insurance company, it is essential to provide detailed and accurate information. Start by supplying your policy number as well as the contact information of all individuals involved in the accident, including their insurance details. Additionally, make sure to mention the location, date, and time of the incident, as these details are crucial for your claim.

Moreover, you should document any evidence from the accident scene. This may include photographs of the vehicles involved, property damage, any visible injuries, and road conditions. Gathering witness statements can also strengthen your position, as they provide third-party insights into the crash. Be as thorough as possible to facilitate a smoother claim process.

Finally, it is important to keep a record of any communication with your insurer. Note the names of representatives you speak with, the time and date of your conversations, and any claim reference numbers. This information can be essential if there are discrepancies in the future or if you need to follow up on your claim.

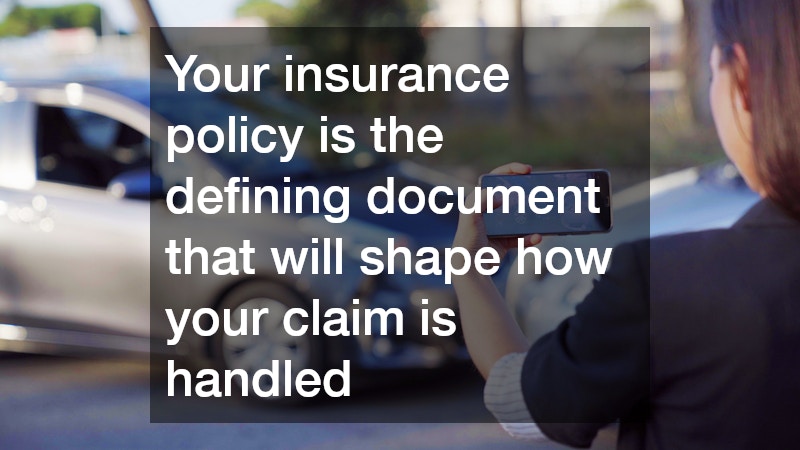

Understand Your Policy

Your insurance policy is the defining document that will shape how your claim is handled post-accident. Familiarize yourself with your specific coverage limits, deductibles, and any clauses regarding collision or comprehensive coverage. Understanding these elements ahead of time can help you manage expectations about what your insurer may be able to provide.

Moreover, it is essential to know whether your policy includes a “no-fault” provision, which can affect how claims are processed in certain states. Under a no-fault system, your own insurance pays for your medical expenses and damages regardless of who is at fault. This can expedite the claim but may limit your ability to recover losses from the at-fault party.

Additionally, your claims history can impact your premiums and eligibility for certain coverage in the future. Frequent claims may lead to higher rates, while a clean driving record might keep rates stable. Understanding this dynamic will help you make informed decisions when dealing with your insurer, especially after a crash.

Avoid Common Mistakes

Filing an auto insurance claim may seem straightforward, but there are common pitfalls that you should avoid to ensure a successful process. One of the most significant mistakes is failing to report the accident promptly. Many insurance policies require that you report incidents within a specific time frame, and delays can result in complications or even denials.

Another pitfall is providing incomplete or inaccurate information during the claims process. Given that the insurer relies heavily on the details you provide, any discrepancies can lead to delays or rejection of your claim. Double-checking the accuracy of your reports and records helps avoid misunderstandings that could jeopardize compensation.

Lastly, many individuals make the mistake of discussing fault at the scene or in their initial report to the insurance company. It is crucial to avoid discussing liability or admitting fault, as this could have significant implications for your claim. Instead, stick to the facts and let the insurance adjusters determine liability based on their findings.

Wait for Processing

The duration of the claims process can vary significantly based on several factors, including the severity of the accident, the complexity of the claims, and the responsiveness of all parties involved. Typically, simpler claims with clear-cut responsibility can be processed relatively quickly, often within a few weeks. However, more complicated situations involving multiple parties may take months to resolve.

The efficiency of your insurance company also plays a considerable role in the claims process timeline. Some insurers are known for their prompt handling of claims, while others may require additional time for reviews and investigations. Understanding the reputation of your insurer regarding claims speed can give you a better idea of what to expect.

Lastly, strive to stay proactive during the claims process. Regularly following up with your claims adjuster and providing any required documentation can expedite your claim’s resolution. An engaged approach can often help mitigate delays and encourage the insurance company to move efficiently towards settling your claim.

Carefully Review Denials

Receiving a denial on your auto insurance claim can be disheartening, but there are steps you can take to address the situation. First, carefully read the denial letter to understand the specific reasons for the rejection. Your insurer is required to provide an explanation for the denial, such as coverage limitations or missing documentation.

Once you understand the reasons behind the denial, gather supporting documentation to strengthen your case. This could include police reports, photographs, and medical records that support your claim. Taking the time to compile evidence can help you challenge the decision effectively.

If you believe your claim was wrongfully denied, don’t hesitate to appeal the insurer’s decision. Most insurance companies have an established process for appeals, and you may need to submit your formal appeal in writing. Ensure that you follow up consistently and keep copies of all correspondence related to your appeal.

Understanding the expectations of auto insurance agencies after a crash is crucial for a smooth claims process. By being well-informed and proactive, you can effectively manage your situation and work towards a fair settlement.